Climate change negatively affects the production systems and producer’s incomes. This study assesses the impact of Village Savings and Loan Associations (VSLA) on strengthening the resilience of vulnerable populations to climate change. Data were collected through focus groups with 41 VSLA and a survey of 210 households VSLA members and non-members, using Holistic Self-Assessment of Peasant Resilience tool. Analysis of variance was applied to the data. The Newman-Keuls test at 5% threshold was used to compare resilience scores, and the chi-square test was applied. The number of VSLA is increasing in Central West region of Burkina Faso. The VSLA of first generation mobilized a yearly average of 1 522 401 F CFA and gave 895 941 F CFA of credits. Their main strengths are solidarity, social cohesion, collect of savings and credit access. VSLA members showed significantly higher resilience scores across social, economic, and environmental domains, particularly in income diversification (p<0.01), land management (p<0.001), and reforestation practices (p<0.001). VSLA contributes significantly to improve social, economic and environmental resilience scores for the vulnerable communities. For the successful operation of VSLA, it’s important to establish partnerships with financial institutions to promote financial inclusion and strengthen actors capacities for more impacts.

| Published in | International Journal of Agricultural Economics (Volume 11, Issue 2) |

| DOI | 10.11648/j.ijae.20261102.11 |

| Page(s) | 29-43 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Association, Burkina Faso, Climate Change, Resilience Score, Savings

Domains | Modules | Componentes | ||||

|---|---|---|---|---|---|---|

Name | Prefix | Noon | Label | Technical score | Self-assessed adequacy | Self-rated importance |

Social | SO | Household | hh | SO-hh-ac-average | SO-hh-adq | SO-hh-imp |

Agronomique | AG | Agricultural practices | agr | AG-agr-ac-average | AG-agr-adq | AG-agr-imp |

Environment | EN | Tree management practices | trees | EN-trees-ac-average | EN-trees-adq | EN-trees-imp |

Economic | EC | Income, expenses and savings | inc | EC-inc-ac- average | EC-inc-adq | EC-inc-imp |

Institutionnal | GO | Policies and programs on climate change | gov | GO-gov-ac- average | GO-gov- adq | GO-gov- imp |

Resilience thresholds | Scale | Signification |

|---|---|---|

Low level of resilience | 0 -7 points | Households have limited capacity to cope with problems in agricultural systems |

Medium level of resilience | 7.01-12 points | Aware of the problems but only partially addressed due to limited or inadequate information, know-how, resources, etc. |

High level of resilience | 12.01-20 points | Problems identified and addressed quickly |

Variables | First generation | Second generation | F | P-value |

|---|---|---|---|---|

Number of cycles completed | 5a ±1 | 3b ± 1 | 49.475 | *** |

Average number of members | 28a ±6 | 26a ± 7 | 1.102 | - |

Average number of abandoned men | 1 a ±1 | 0b | 6.041 | * |

Average share value (FCFA) | 273 a ± 113 | 345 a ± 131 | 3.514 | - |

Average share amount (FCFA) | 1 212 862a ±763 672 | 1 308 731a ±620 073 | 0,157 | - |

Average total amount of solidarity at closing (FCFA) | 79330 a ± 48 044 | 54 355 a ± 49 880 | 2.606 | - |

Average amount of men's credits (FCFA) | 206818 a ± 23519 | 47 526 b ± 11 422 | 6.304 | * |

Average amount of credits for women (FCFA) | 693290 a ±143105 | 400 508a ± 68 293 | 0.578 | - |

Average amount of member credits (FCFA) | 895 941a ± 139 940 | 521523a ± 76307 | 0.951 | - |

Average amount mobilized (FCFA) | 1 522 401 a ±1 238 515 | 1338156 a ±494 515 | 0.318 | - |

Average amount total received per member (FCFA) | 51 882 a ±43 359 | 45 115a ±25 512 | 0.094 | - |

First generation | Second generation | Total | p-value | |

|---|---|---|---|---|

Sex of President for the last cycle completed | ** | |||

Man | 39.02 | 12.20 | 51.22 | |

Woman | 19.51 | 29.27 | 48.78 | |

Purchase between 1 and 5 shares at each meeting | - | |||

Yes | 48.78 | 36.59 | 85.37 | |

Payment of mandatory penalties | - | |||

Yes | 56.1 | 41.46 | 97.56 | |

Solidarity amount set by the Internal Regulations (RI) | - | |||

Yes | 58.54 | 36.59 | 95.12 | |

The maximum loan amount is equal to 3 times the value of the savings | - | |||

Yes | 21.95 | 12.2 | 34.15 | |

Loans repaid within a maximum of 3 months | *** | |||

No | 0 | 17.07 | 17.07 | |

Yes | 58.54 | 24.39 | 82.93 | |

Cumulative credits | - | |||

Yes | 19.51 | 12.2 | 31.71 | |

All credits recovered at the end of each cycle | - | |||

Yes | 52.63 | 39.47 | 92.11 | |

3 plastic bowls of different colors, at least 30 cm in diameter and 15 cm deep | *** | |||

No | 9.76 | 36.59 | 46.34 | |

Yes | 48.78 | 4.88 | 53.66 | |

VSLA saves in a licensed financial institution | - | |||

Yes | 21.95 | 14.63 | 36.59 |

Variables | Non VSLAs (n = 105) | VSLAs (n = 105) | F | P-value | |

|---|---|---|---|---|---|

SOCIAL | SO_HH_RES- HOUSEHOLD | 12.6 a±2 | 12.6 a±2 | 0.107 | - |

SO_group_res- GROUP MEMBERSHIP | 5.4 a± 4.3 | 6.5 a±4.3 | 3.056 | - | |

SO_coop_res- COMMUNITY COOPERATION | 13.4 a± 2.7 | 13.6 a± 2.7 | 0.006 | - | |

SO_dmhh_res- HOUSEHOLD DECISION-MAKING | 11.6 a± 2.3 | 11.4 a± 2.3 | 0.257 | - | |

SO_meal_res-ALIMENTATION | 10.9 a± 3.5 | 10.8 a± 3.5 | 0.112 | - | |

AGRONOMIC | EN_crop_res-CROP PRODUCTION | 9b± 3.3 | 10.1 a± 3.3 | 5.672 | * |

SO_agr_res- AGRICULTURAL PRODUCTION ACTIVITIES | 8.1 a±3.5 | 9a±3.5 | 3.146 | - | |

EN_animal_res- ANIMAL PRODUCTION PRACTICES | 10.6 a± 2.4 | 11.3 a±2.4 | 3.696 | - | |

SO_landac_res- ACCESS TO LAND | 10.7a± 2.4 | 10,7 a± 2.4 | 0.886 | - | |

SO_infoac_res- ACCESS WEATHER INFO AND ADAPT CC | 9 a±3.8 | 9.4 a±3.8 | 0.656 | - | |

SO_ict_res- INFORMATION & COMMUNICATION TECHNOLOGY | 15.9 a± 1.8 | 15.7 a± 1,8 | 0.505 | - | |

ECONOMICAL | EC_input_res-AGRICULTURAL INPUT | 10.2 a±3.3 | 10.6 a±3.3 | 0.794 | - |

EC_mkt_res- MARKETS ACCESS | 10.3 a±2 | 10.8 a±2 | 0.843 | - | |

EC_inc_res- SOURCES OF INCOME/EXPENSES/SAVINGS | 9.7 b±3 | 10.9 a±3 | 8.288 | ** | |

EC_ass_res- MAIN MEANS OF PRODUCTION | 12 a±3.4 | 12.4 a± 3.4 | 0.6 | - | |

EC_fin_res- ACCESS TO FINANCIAL SERVICES | 13.7 a± 1.6 | 12.6 a± 1.6 | 2.758 | - | |

EC_ins_res- INSURANCE | 17.5 a± 1.3 | 16.3 a± 1.3 | 1 | - | |

ENVIRONNMENTAL INSTITUTIONNAL | EN_slm_res LAND MANAGEMENT | 14.8 b± 2,6 | 16 a±2.6 | 12.716 | *** |

EN_wacc_res WATER ACCESS AND MANAGEMENT | 12.4 a±1.4 | 12.4 a±1.4 | 0.031 | - | |

EN_trees_res TREES | 11.5 b± 1.8 | 12.4 a± 1.8 | 13.509 | *** | |

EN_cc_res DISTURBANCE | 3.9 b±3.1 | 5.1 a±3.1 | 7.852 | ** | |

GO_gov_res_ GOVERNANCE | 14.5 a± 2.3 | 14.4 a± 2.3 | 0.019 | - |

ANAM-BF | National Agency of Meteorology |

ANOVA | Analysis of Variance |

CdR | Resilience Fund |

CoBRA | Community Resilience Assessment and Action |

FAO | Food and Agriculture Organization of the United Nations |

GDP | Gross Domestic Product |

GEF | Global Environment Facility |

HDI | Human Development Index |

IGAs | Income-Generating Activities |

INSD | National Institute of Statistic and Demography |

NGOs | Non-Governmental Organizations |

ODK | Open Data Kit |

REAL | Resilience Evaluation, Analysis and Learning |

RIMA | Resilience Index Measurement and Analysis |

SHARP | Holistic Scheme for Self-Assessment of Climate Resilience |

UN | United Nations Agencies |

UNDP | United Nation Development Programme |

VSLA | Village Savings and Loan Associations |

| [1] | IPCC. Climate Change: Synthesis Report. Contribution of Working Groups I, II and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, H. Lee and J. Romero (eds.)]. IPCC, 2023, Geneva, Switzerland, 184 pp., |

| [2] | Roncoli C, Ingram K, Kirshen P. «the costs and risks of coping with drought: livelihood impact and farmers’ responses in Burkina Faso», In Climate research, 19, 2001, pp. 119-132. |

| [3] | Brou Y T., Akindes F., Bigot S. «Climate variability in Côte d'Ivoire: social perceptions and agricultural responses», In Cahiers Agricultures. 2005, 14(6): 533-540. |

| [4] | Ministry of Economy, Finance and Forecasting (MEFP). National accounts for 2023 (First estimates based on the CNTs), 2023, 11 p. |

| [5] | PNSR II. Second National Rural Sector Programme (PNSR), 2017, 70 p. |

| [6] |

CONASUR. National multi-hazard plan for disaster preparedness and response, 2012, Available from:

https://www.preventionweb.net/publication/burkina-faso-plan-nationalmulti-risques-de-preparation-et-de-reponse-aux-catastrophes (accessed 20 October 2025). |

| [7] | Sidibe H, Diallo M et Barry C. «Pulaaku and identity crisis: the case of the Red Fulani of the Issa-Ber lake region in Mali» In Fulani identity; Paris, Karthala, 1997, pp. 223-240. |

| [8] |

Soulama A. Floods in Burkina Faso in early September, 2009. Available from:

https://www.mediaterre.org/afrique_ouest/actu.html (accessed 22 August 2025). |

| [9] | National Meteorological Agency (ANAM-BF). Ten-day agro-meteorological bulletin n 28, 2022, 11 p. |

| [10] | United Nations Development Programme (UNDP). Human Development Report, 2022, 8 p. |

| [11] | Ministry of the Economy, Finance and Forecasting (MEFF). Main findings of the study on poverty and household living conditions, 2021, 8 p. |

| [12] | National Institute of Statistics and Demography (NISD). Multi-sectoral survey: Savings and access to credit, 2015, 73 p. |

| [13] | CARE. Micro-savings: a development tool for populations excluded from microfinance., 2013, 13 p. |

| [14] | Kaire A.K., Sow S. et Balde S. The effects of microcredit on strengthening the socioeconomic power of women members of the Village Savings and Credit Associations (VSLAs) of the Commune of Sahm Notary. Int. J. Econ. Stud. Manag. 2022, 2, No. 3. 473-488 |

| [15] | Eclosio. Village Savings and Credit Associations (VSLAs): A tool for strengthening the economic empowerment of Beninese women farmers. ANAF-Benin, 2016, 3 p. |

| [16] | Ndabarushimana A. & Niyokwizzera E. Role of Save Our Souls (SOS) Children's Villages Burundi in the Community Development Process: The Case of Village Savings and Loan Associations (VSLAs) Initiated by its Program for Improving the Living Conditions of Households in Bujumbura. ESI Preprints, 2022, 339 p. |

| [17] | Fall K. Organization and Dynamics of Solidarity in Rural Areas: The Example of Village Savings and Credit Associations (VSLAs), Scientific Journal of the Alassane Ouattara University. 2021. Vol. 1 -. 40 p. |

| [18] | Champchesnel M. F., Fioekou C., Sanda H B., Lavaur A-L, Mayans J. Village Savings and Credit Associations: an approach adapted to the poorest households? Characteristics of members and impact on household economies. Clichy France, 2016, 36 p. |

| [19] |

Choptiany J., Graub B., Phillips S., Colozza D. & Dixon J. Self-evaluation and holistic assessment of climate resilience of farmers and pastoralists. Rome, FAO, 2015.

http://www.fao.org/3/i4495e/i4495e.pdf (accessed 20 October 2025). |

| [20] | RGPH. Monograph of the Central-Western Region, 2019, 181 p. |

| [21] | Central West Regional Development Plan, 2017-2021, 2017, 169 p. |

| [22] | Coordination Sud. Adaptation and resilience to climate change: Review of metrics and monitoring indicators, 2022, 43 p. |

| [23] | Lagana H, M., Phillips, S. and Poisot, A. Self-evaluation and holistic assessment of climate resilience of farmers and pastoralists (sharp+) – A new guidance document for practitioners. Rome, FAO. 2022. |

| [24] | Carpenter S., Walker B., Anderies J. M. & Abel N. From metaphor to measurement: Resilience of what to what? Ecosystems. 2001, 4(8): 765–781, |

| [25] | Walker B., Holling C. S., Carpenter S. R. & Kinzig A. Resilience, adaptability and transformability in social-ecological systems. Ecology and Society. 2004, 9(2): 5 |

| [26] | Cabell, J. F., and M. Oelofse. An indicator framework for assessing agroecosystem resilience. Ecology and Society. 2012, 17(1): 18. |

| [27] | Kouadio Sarah. Village savings and credit associations and empowerment: a socio-economic analysis, 2020, 16 p. |

| [28] | United Nations Framework Convention on Climate Change (UNFCCC). Contribution to the World Summit on Sustainable Development, Conference of the Parties, Seventh Session, Marrakech, 2001, 10 p. |

| [29] | Christopher Ksoll, Helene Bie Lilleør, Jonas Helth Lønborg, Ole Dahl Rasmussen. Impact of Village Savings and Loan Associations: Evidence from a cluster randomized trial. Journal of Development Economics 120 (2016) 70–85. |

| [30] |

Agrifarm. Village Savings and Loan Associations (VSLAs): An essential lever for women's empowerment in Africa, 2015,

https://agrifambenin.wordpress.com/2025/03/15/c accessed on february, 10th, 2026. |

APA Style

Koutou, M., Thiombiano, B. A., Karambiri, S., Souli, S., Ilboudo, S., et al. (2026). Impact of Village Savings and Loan Associations on Improving the Resilience of Vulnerable Populations to Climate Change in the Central West Region of Burkina Faso. International Journal of Agricultural Economics, 11(2), 29-43. https://doi.org/10.11648/j.ijae.20261102.11

ACS Style

Koutou, M.; Thiombiano, B. A.; Karambiri, S.; Souli, S.; Ilboudo, S., et al. Impact of Village Savings and Loan Associations on Improving the Resilience of Vulnerable Populations to Climate Change in the Central West Region of Burkina Faso. Int. J. Agric. Econ. 2026, 11(2), 29-43. doi: 10.11648/j.ijae.20261102.11

AMA Style

Koutou M, Thiombiano BA, Karambiri S, Souli S, Ilboudo S, et al. Impact of Village Savings and Loan Associations on Improving the Resilience of Vulnerable Populations to Climate Change in the Central West Region of Burkina Faso. Int J Agric Econ. 2026;11(2):29-43. doi: 10.11648/j.ijae.20261102.11

@article{10.11648/j.ijae.20261102.11,

author = {Mahamoudou Koutou and Boundia Alexandre Thiombiano and Souleymane Karambiri and Salamata Souli and Stephane Ilboudo and Kossi Sena Adufu and Patrice Toe},

title = {Impact of Village Savings and Loan Associations on Improving the Resilience of Vulnerable Populations to Climate Change in the Central West Region of Burkina Faso},

journal = {International Journal of Agricultural Economics},

volume = {11},

number = {2},

pages = {29-43},

doi = {10.11648/j.ijae.20261102.11},

url = {https://doi.org/10.11648/j.ijae.20261102.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijae.20261102.11},

abstract = {Climate change negatively affects the production systems and producer’s incomes. This study assesses the impact of Village Savings and Loan Associations (VSLA) on strengthening the resilience of vulnerable populations to climate change. Data were collected through focus groups with 41 VSLA and a survey of 210 households VSLA members and non-members, using Holistic Self-Assessment of Peasant Resilience tool. Analysis of variance was applied to the data. The Newman-Keuls test at 5% threshold was used to compare resilience scores, and the chi-square test was applied. The number of VSLA is increasing in Central West region of Burkina Faso. The VSLA of first generation mobilized a yearly average of 1 522 401 F CFA and gave 895 941 F CFA of credits. Their main strengths are solidarity, social cohesion, collect of savings and credit access. VSLA members showed significantly higher resilience scores across social, economic, and environmental domains, particularly in income diversification (p<0.01), land management (p<0.001), and reforestation practices (p<0.001). VSLA contributes significantly to improve social, economic and environmental resilience scores for the vulnerable communities. For the successful operation of VSLA, it’s important to establish partnerships with financial institutions to promote financial inclusion and strengthen actors capacities for more impacts.},

year = {2026}

}

TY - JOUR T1 - Impact of Village Savings and Loan Associations on Improving the Resilience of Vulnerable Populations to Climate Change in the Central West Region of Burkina Faso AU - Mahamoudou Koutou AU - Boundia Alexandre Thiombiano AU - Souleymane Karambiri AU - Salamata Souli AU - Stephane Ilboudo AU - Kossi Sena Adufu AU - Patrice Toe Y1 - 2026/03/16 PY - 2026 N1 - https://doi.org/10.11648/j.ijae.20261102.11 DO - 10.11648/j.ijae.20261102.11 T2 - International Journal of Agricultural Economics JF - International Journal of Agricultural Economics JO - International Journal of Agricultural Economics SP - 29 EP - 43 PB - Science Publishing Group SN - 2575-3843 UR - https://doi.org/10.11648/j.ijae.20261102.11 AB - Climate change negatively affects the production systems and producer’s incomes. This study assesses the impact of Village Savings and Loan Associations (VSLA) on strengthening the resilience of vulnerable populations to climate change. Data were collected through focus groups with 41 VSLA and a survey of 210 households VSLA members and non-members, using Holistic Self-Assessment of Peasant Resilience tool. Analysis of variance was applied to the data. The Newman-Keuls test at 5% threshold was used to compare resilience scores, and the chi-square test was applied. The number of VSLA is increasing in Central West region of Burkina Faso. The VSLA of first generation mobilized a yearly average of 1 522 401 F CFA and gave 895 941 F CFA of credits. Their main strengths are solidarity, social cohesion, collect of savings and credit access. VSLA members showed significantly higher resilience scores across social, economic, and environmental domains, particularly in income diversification (p<0.01), land management (p<0.001), and reforestation practices (p<0.001). VSLA contributes significantly to improve social, economic and environmental resilience scores for the vulnerable communities. For the successful operation of VSLA, it’s important to establish partnerships with financial institutions to promote financial inclusion and strengthen actors capacities for more impacts. VL - 11 IS - 2 ER -

Department of Agricultural and Environmental Sciences, University Center of Tenkodogo (CUT), Tenkodogo, Burkina Faso;Department of Rural Sociology and Economics, Institute of Rural Development (IDR), Bobo Dioulasso, Burkina Faso

Biography: Mahamoudou Koutou is an experienced specialist in Agricultural economic and climate change. He completed his PhD in Agricultural economics from Abomey Calavi University (Benin) in 2018, and his engineer in rural development from Nazi Boni University (Burkina Faso) in 2006 and Master of natural resources management from the same institution in 2008. He completed also his Master of agricultural innovations from Joseph Ki-Zerbo University (Burkina Faso) in 2010. He worked as researcher on food security project at International Research and Development Center on Livestock Farming in Subhumid Zones (CIRDES) for 8 years and at FAO as monitoring and evaluation expert, agricultural value chain expert, climate change expert for 7 years. He is a member of Laboratory for Rural Studies on the Environment and Economic and Social Development (LERE/DES). He has participated in multiple international conference in recent years. He currently serves as a consultant at FAO on policy reform and contribute as reviewer of the African Journal of Food, Agriculture, Nutrition and Development.

Research Fields: Agricultural Economics, Climate change resilience, Agricultural value chain, Impact assessment, Agricultural innovations co-conception, Agricultural innovations diffusion, Food and agricultural policies, Market analysis

Department of Rural Sociology and Economics, Institute of Rural Development (IDR), Bobo Dioulasso, Burkina Faso

Biography: Boundia Alexandre Thiombiano is an Associate professor at Nazi Boni University, Rural development Engineering Department. He completed his PhD in Agricultural Economics from Kwamé NKrumah university of science and technology (Ghana) in 2015, and his Master of Engineering in rural development from Nazi Boni University in 2010. He has Over 15 years of cumulative experience in research and development, Consulting firms, Government structures (Ministry, State-owned company, Multilateral programs, United Nations system organizations (UNHCR). He led Burkina Phosphate Mining Company for 3 years. He currently serves as Director of rural sociology and economy department at Nazi Boni University and contribute as reviewer in numerous journals. He has been invited as a Keynote Speaker, Technical Committee Member, Session Chair, and Judge at international conferences. He has participated in multiple international conference in recent years. He is a member of Laboratory for Rural Studies on the Environment and Economic and Social Development (LERE/DES).

Research Fields: Climate change, Climate vulnerability analysis, Agricultural Economics, Agricultural Value Chain, Sustainable development

Cultures and Tourism Department, Sib Sié Faustin University, Gaoua, Burkina Faso

Biography: Souleymane Karambiri is a Lecturer and Researcher in Sociology. He completed his PhD in sociology of development from Joseph Ki-Zerbo University (Burkina Faso). His research interests focus primarily on land tenure, migration, territorial dynamics, public policy, urban agriculture, and agricultural innovation. He is a member of the CAMES Thematic Research Program on Governance and Democracy (PTR-GD/CAMES), the Laboratory for Society, Mobility and Environment (LASME), and the Laboratory for Rural Studies on the Environment and Economic and Social Development (LERE/DES). He has participated in multiple international conference

Research Fields: Land management, land tenure, migration, territorial dynamics, public policy, urban agriculture, and agricultural innovation

Department of Rural Sociology and Economics, Institute of Rural Development (IDR), Bobo Dioulasso, Burkina Faso

Biography: Salamata Souli is a student in Master degree at Nazi Boni University (Burkina Faso), rural sociology and economy Engineering Department. She completed her Master in 2025. She is preparing for PhD student program in climate change. She is a member of Laboratory for Rural Studies on the Environment and Economic and Social Development (LERE/DES). She contributed for data collection in the team.

Research Fields: Agricultural Economics, Climate change resilience, Agricultural value chain, Impact assessment, rural economy

Office for Studies, Research and Support-Advice for Local Initiatives (BERACIL), Ouagadougou, Burkina Faso

Biography: Stephane Ilboudo is a geomatician and geographer at Bureau for Studies, Research and Support-Consulting for Local Initiatives (BERACIL). He completed his Master of geography from Joseph Ki-Zerbo University (Burkina Faso). He currently serves as the technical advisor. It provides advisory support to rural communities and community-based businesses through training, guidance on structuring and organization, and orientation towards promising sectors. Its actions also focus on supporting the drafting of development projects, the creation of business plans and company development plans, as well as monitoring progress.

Research Fields: Geomatician, geography, Geomarketing, sociology, Sustainable Agriculture, Agricultural value chain

Emergency and Resilience Unit, Food and Alimentation Organization (FAO), Accra, Ghana

Biography: Kossi Sena Adufu is a Programme & Operation Expert at FAO Africa Regional Office in Accra, Ghana. He completed his Master in Agricultural economics from university of Lome (Togo). He has been worked with FAO for over 20 years. He is a designer of Village Savings and Loan Associations, resilience fund. He has participated in multiple international research collaboration projects in recent years. He published several useful book in human well-being and agricultural sector. He has been invited as a Keynote Speaker, Technical Committee Member, Session Chair, and Judge at international conferences.

Research Fields: Agricultural Economics, Climate change resilience, Agricultural value chain, Impact assessment, Village Savings and Loan Associations, resilience fund

Department of Rural Sociology and Economics, Institute of Rural Development (IDR), Bobo Dioulasso, Burkina Faso

Biography: Patrice Toe is a Full Professor of Socio-Anthropology at the Institute of Rural Development (IDR)/Nazi Boni University of Bobo-Dioulasso (UNB), where he has served successively as Head of the Department of Rural Sociology and Economics, Director of External Relations, and Deputy Director of the Doctoral School. Currently, he is Director of the Laboratory for Rural Studies on the Environment and Economic and Social Development (LERE/DES) and doctoral school and leads the research area "Heritage, Societies, and Development." He completed his PhD in sociology of development and and anthropology. His recent work focuses on the issues of "sustainable water resource management" and "strategies of local actors in the face of health research on biomedical technologies."He is a member of the International Scientific Committee of the African Center of Excellence in Technological Innovations for the Elimination of Vector-Borne Diseases (CEA-ITECH-MTV), he is the Scientific Coordinator of the Center's Master's program in "Ecosystems, Health, and Societies."He has been invited as a Keynote Speaker, Technical Committee Member, Session Chair, and Judge at international conferences.

Research Fields: Sustainable Agriculture, rural sociology, sustainable water resource management, strategies of local actors, biomedical technologies

Figure 1. Location of the study area.

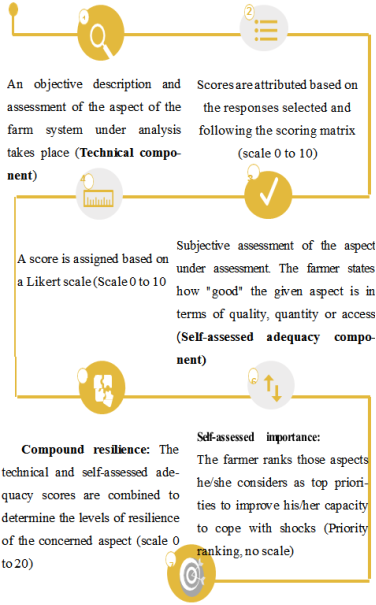

Figure 2. Flowchart explaining how resilience levels and priority areas are defined in SHARP+ (Source: [21]).

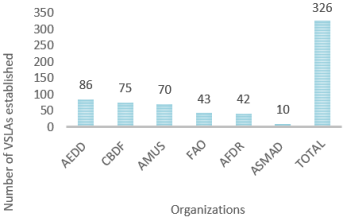

Figure 3. Village savings and credit associations established by organizations in the Central-West region.

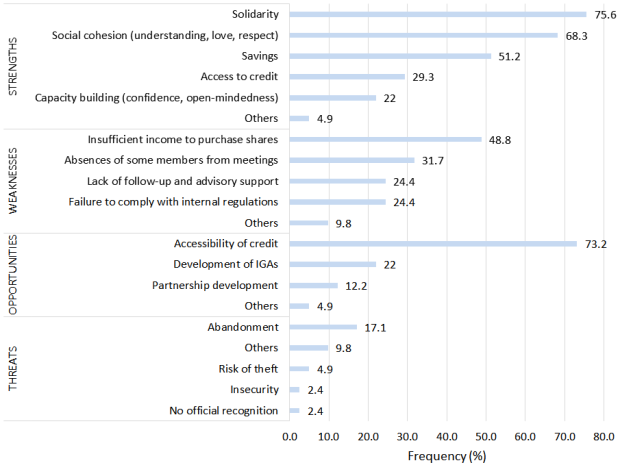

Figure 4. Strengths, weaknesses, opportunities and threats of VLSAs according to members.

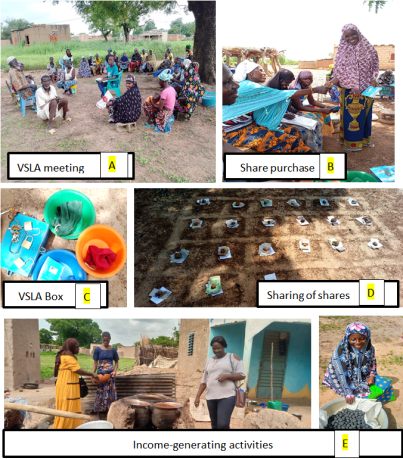

Figure 5. Illustrative photos of how VSLAs work.